Capital Gains Section 67 Decoded | CA Final May 2027

March 2026 · The May 2027 Transition Series — Part 7 · 10 min read

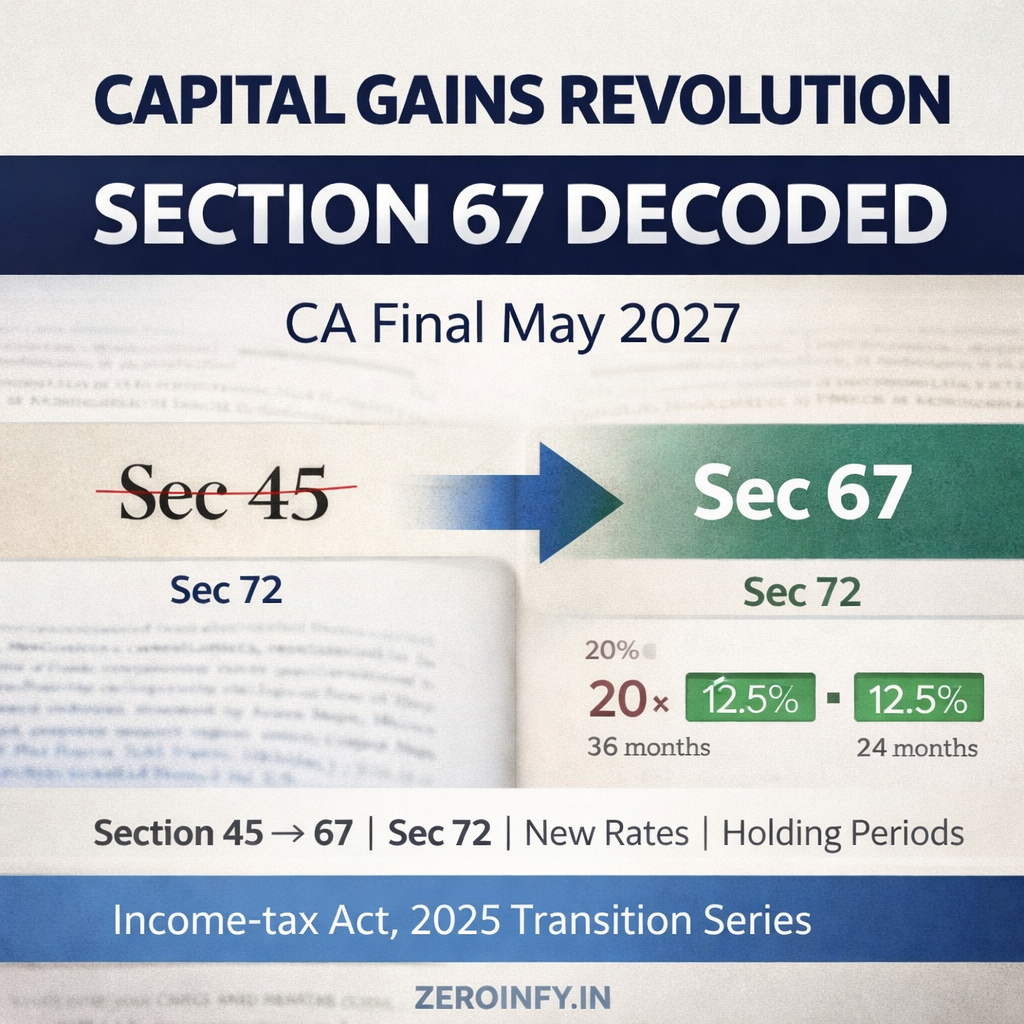

Capital Gains is the most dynamic chapter in Direct Tax — every Budget tweaks it. For May 2027, the entire legal foundation has shifted. Section 45 is gone. Section 67 is in. The rates have changed. The holding periods have changed. And the computation formula has been rewritten. This is your complete guide.

1. The Big Move: Section 45 → Section 67

Under the 1961 Act, Section 45 was the charging section for Capital Gains — the provision that brought profits from asset transfers into the tax net. Under the Income-tax Act, 2025, this charge now sits at Section 67, placed in Chapter VII — Capital Gains.

This is not just a renumbering. The new section consolidates several deeming provisions that were scattered across the old Act into one clean, structured section. For the May 2027 exam, citing Section 45 is citing a repealed law.

Sec 45

Old Act, 1961

Scattered across Sections 45–55A

→

Sec 67

New Act, 2025

Chapter VII — unified, structured, 18 sub-sections

| Provision | Old Act (1961) | New Act (2025) |

|---|---|---|

| Charging Section | Section 45 | Section 67 New |

| Computation | Section 48 | Section 72 New |

| Exemptions from CG | Section 47 | Section 70 New |

| Cost of Acquisition | Section 49 | Section 73 New |

| STCG (STT paid equity) | Section 111A @ 15% | Section 196 @ 20% Changed |

| LTCG (General) | Section 112 @ 20% (with indexation) | Section 197 @ 12.5% Changed |

| LTCG (STT paid equity) | Section 112A @ 10% (above ₹1L) | Section 198 @ 12.5% (above ₹1.25L) Changed |

| Buy-back of Shares | Section 46A | Section 69 New |

2. Section 67(1) — The Charging Provision

Section 67(1) states: any profits or gains arising from the transfer of a capital asset effected in a Tax Year shall be chargeable to income-tax under the head “Capital Gains” and shall be deemed to be the income of the Tax Year in which the transfer took place.

Three words in this section carry the entire weight of the chapter:

🔑

“Transfer”

Defined in Sec 2(109). Includes sale, exchange, relinquishment, extinguishment of rights, compulsory acquisition. Critical — no transfer = no CG.

🏠

“Capital Asset”

Property of any kind — movable, immovable, tangible, intangible. Exceptions: stock-in-trade, personal movables, agricultural land (rural).

📅

“Tax Year”

The year of transfer is the year of chargeability. Under the old Act this was “Previous Year.” New Act uses Tax Year — same concept, new name.

3. Holding Period — STCA vs LTCA

The classification of an asset as Short-Term or Long-Term determines the tax rate, indexation benefit, and exemption eligibility. Under Section 2(101), the holding period rules are:

| Asset Type | STCA (held ≤) | LTCA (held >) |

|---|---|---|

| Listed equity shares / equity MF units / units of business trust / zero coupon bonds | 12 months | > 12 months |

| All other assets (land, building, unlisted shares, gold, debt MF, etc.) | 24 months | > 24 months |

💡

Exam Insight — 24-Month Rule is the Default

The 24-month rule is the general rule under Sec 2(101)(a). The 12-month rule is the exception for listed securities/equity MF/ZCB only — per Sec 2(101)(b). In the exam, if an asset type is not specified, always apply 24 months. Immovable property, unlisted shares, gold — all follow 24 months.

4. Computation — Section 72

Section 72 (old Section 48) is where the actual CG number is computed. The formula is:

Capital Gains Computation — Sec 72(1)

A

Full Value of Consideration received or accruing on transfer

−

Expenditure incurred wholly and exclusively in connection with the transfer

−

Cost of Acquisition + Cost of Improvement (or Indexed cost for LTCG on eligible assets)

= Capital Gains (chargeable under head “Capital Gains”)

⚠️

Key Restriction — Sec 72(3)

Two deductions are NOT allowed under Section 72: (a) Interest claimed as deduction under Section 22(1)(b) or Chapter VIII, and (b) Securities Transaction Tax paid. These are perennial exam traps — students often deduct STT. It is expressly disallowed.

5. Tax Rates — The Biggest Change for May 2027

This is the area students are most likely to get wrong in the exam. The Finance Act, 2024 amendments (effective 23rd July, 2024) have been carried into the 2025 Act. Rates have changed significantly from what most students studied.

⚠ Critical Exam Alert — Rate Changes Students Get Wrong

STCG (equity): NOT 15% anymore — it is 20% under Sec 196

LTCG (equity): NOT 10% anymore — it is 12.5% under Sec 198

LTCG (general): NOT 20% with indexation — it is 12.5% without indexation under Sec 197

Exemption limit (Sec 198): NOT ₹1L — it is ₹1.25L

6. Key Deeming Provisions Inside Section 67

Section 67 consolidates several special rules that were scattered across the old Act. These sub-sections are favourite exam questions:

7. The Articleship Re-Label Exercise

Every capital gains computation you’ve done in practice is conceptually valid. Just update your section references:

8. Exam Strategy for May 2027

Computation Question (15–20 marks): Always follow the Sec 72(1) formula — Full Value of Consideration minus Transfer Expenses minus Cost of Acquisition/Improvement. Then classify as STCG or LTCG using holding period. Apply the correct rate from Sec 196 / 197 / 198. Never deduct STT — Sec 72(3) expressly bars it.

Theory Question (4–6 marks): For JDA, compulsory acquisition, or conversion questions — always identify the correct sub-section of Sec 67, state the deeming fiction, and identify what constitutes the “full value of consideration.” That three-part answer always scores full marks.

🚀

Strategic Exam Tip for May 2027

Every CG answer should end with a tax rate conclusion. State: “Since the asset is a [long-term / short-term] capital asset, the capital gains of ₹X are chargeable under Section [196 / 197 / 198] of the Income-tax Act, 2025 at [20% / 12.5%].” Citing the correct new section number instead of the old one signals to the examiner that you are May 2027 ready.

📥 Download the Capital Gains Quick Reference Chart

Section 67 vs Section 45 · Holding Periods · Tax Rates (Sec 196/197/198) · Key Deeming Provisions — all on one page.

📚 The May 2027 Transition Series

Master the New Income-tax Act, 2025 with our comprehensive 7-part guide:

Source link

You may also like

The E-Learning Basics